Seeking Alpha: How Sprint & Clearwire Can Use AT&T to Unlock Billions in Value

Entry posted by S4GRU

3,053 views

An article was posted on the Seeking Alpha website titled, "How Sprint & Clearwire Can Use AT&T to Unlock Billions in Value." It's a very interesting read that went over details why it would be wise for Sprint to buy Clearwire out right. This is something I never would have ever recommended before reading the article.

An article was posted on the Seeking Alpha website titled, "How Sprint & Clearwire Can Use AT&T to Unlock Billions in Value." It's a very interesting read that went over details why it would be wise for Sprint to buy Clearwire out right. This is something I never would have ever recommended before reading the article.

It's a long read, but raises some very interesting points. If Sprint could master a Clearwire buy out in a way exactly as mentioned in the article, it could work and be very beneficial for the company.

However, even the best laid plans...

UPDATE: The article was taken down by Seeking Alpha for some reason. Conspiracy, perhaps? Either way, I was able to get the data from the article in a Google Search cache, thankfully. I have reposted below.

QuoteHow Sprint & Clearwire Can Use AT&T to Unlock Billions in ValueNow that the AT&T and T-Mobile merger has finally collapsed, investors are left wondering about the implications this has for the US wireless industry. We believe that the collapse of this deal presents a unique opportunity for both Sprint (S) and Clearwire (CLWR). But before we examine how Sprint and Clearwire can unlock shareholder value from this development, we must first examine recent developments in the wireless industry.

We have always believed that the merger between AT&T and T-Mobile was not as much of a threat to Sprint as either Sprint or Wall Street made it out to be. The disappearance of T-Mobile would allow Sprint to position itself as the only national low cost carrier, something that it is now unable to do. In addition, T-Mobile has been given $3 billion in cash, spectrum in 128 markets, and a 7 year roaming deal for its troubles in attempting to merge with AT&T. This reinvigorated T-Mobile will be able to compete more aggressively than before, at least in the short term. Though T-Mobile is reinvigorated for now, we believe that it is just as vulnerable in the long run.

With T-Mobile being left without a partner, its long term position has weakened. Though it is infused with billions from AT&T's breakup fee, T-Mobile has billions in upcoming expenses associated with its network upgrade, and it is short on spectrum, a problem AT&T must address as well. While AT&T was busy saving its merger with T-Mobile, it missed a prime opportunity to acquire spectrum from a consortium of cable companies, thus allowing Verizon to swoop in and do so instead. Verizon paid $3.6 billion to Comcast, Time Warner, and BrightHouse Networks. Verizon made another spectrum buy last Friday, buying Cox's own spectrum for $315 million. Despite a government probe into the transaction, we think the deal will remain in place, for the following reasons:

- Competition: The cable companies were never meaningful players in the wireless market, and as such their exit does not meaningfully alter the competitive landscape. There was never any indication that Comcast, BrightHouse, or Time Warner Cable were going to develop their own wireless networks, and now this unused spectrum is actually being used.

- The FCC supports the use of unused spectrum: Because it is up to Congress to initiate spectrum auctions, they are rare occurrences. As such, spectrum must be bought elsewhere. The FCC has called on Congress to initiate more auctions. As the marketplace waits for more spectrum to be auctioned, demand for it is only growing. It is no secret that Verizon needs spectrum, and if it cannot get it from the government's auctions, it must acquire it somewhere. The FCC wants Verizon to be able to provide faster service to its customers. In order to do so, Verizon needs this spectrum. According to Jeff Silva, senior policy director at Medley Global Advisors, "the FCC and Justice Department are likely to approve the deal, though they may require the sale of assets in certain markets."

- Possible divestitures and concessions: As part of their agreement, Verizon and the cable companies will become partners , selling each other's services. Verizon will resell cable services in its stores, receiving a cut of all the sales, and the cable companies will resell Verizon's wireless services, receiving a cut of those sales. Competition concerns have arose because of this partnership, and we think Verizon would be ready and willing to terminate it to retain control of the spectrum, something that is far more important than reselling services. If the companies do not resell each other's services, they go back to being competitors, and the cable companies have $3.6 billion more to invest in their businesses.

As soon as the announcement of the AT&T/T-Mobile merger collapse broke, analysts began speculating over what both companies will do next. Analysts are speculating that T-Mobile may wind up combining with Sprint, something we see no sense in, for several reasons.

- Incompatible networks: Sprint has already been through one incompatible network merger, the scars of which are still visible. The disastrous merger with Nextel saddled the Sprint with billions in losses, and we do not think Dan Hesse will make that mistake again. Running T-Mobile and Sprint as a combined company will be far too cumbersome, in our opinion, for it to be worthwhile.

- Deutsche Telekom still has T-Mobile: Merging T-Mobile and Sprint would likely mean that Deutsche Telekom receives a stake in the combined company, not cash. That runs counter to what the Deutsche Telekom wishes to do. Having a stake in Sprint/T-Mobile means continuing to invest in it, and Deutsche Telekom wants to be rid of T-Mobile and focus on its other markets.

- Hypocrisy and anti-trust: No one has been a more vocal opponent of the AT&T/T-Mobile deal than Sprint. In its statement on the merger's collapse, Sprint said that , "from the beginning, Sprint has stood with consumers who spoke loudly and clearly that AT&T’s proposed takeover of T-Mobile would create an undeniable duopoly that would have resulted in higher prices, less innovation and fewer choices for the American consumer." It would be the height of hypocrisy for Sprint to so vehemently oppose the merger of AT&T and T-Mobile, and then agree to merge with T-Mobile itself. Furthermore, anti-trust issues would still remain. The government has made it clear that it wants 4 national wireless companies in the market, not 3.

Since merging with Sprint does not provide a solution to T-Mobile's spectrum needs, several analysts have suggested a partnership with Clearwire (CLWR). Clearwire, while wholly dependent on Sprint, has made no secret of its desire to diversify away from its primary backer, and partnering with T-Mobile could be beneficial to Clearwire. But while we see the benefits of such a deal for Clearwire, we do not see a long term benefit for Deutsche Telekom, which is still left with T-Mobile in such a scenario. Deutsche Telekom is facing enormous pressures across many of its divisions, and wanted to use the proceeds of the T-Mobile sale to improve its balance sheet . Furthermore, we think this merger runs counter to Deutsche Telekom's other priorities. Deutsche Telekom is facing billions in spending on its European business, as well as preserving its own dividend and we think that the only long term solution Deutsche Telekom has is to sell T-Mobile to someone, be they a consortium of minor wireless companies, or a private equity fund. However, the recent reshaping of the wireless landscape has the potential to dramatically alter Clearwire's fortunes, if Clearwire makes the right moves.

Just as analysts have rushed to speculate about what T-Mobile will do, analysts have begun to generate potential scenarios of AT&T's future, and many involve Clearwire. Without T-Mobile, AT&T is still in need of spectrum, and it has made fewer spectrum deals than Verizon. AT&T's last major spectrum transaction was a $2 billion deal with Qualcomm (QCOM), announced in November 2011. The sale is still pending before the FCC, and it will take another $1 to $2 billion to integrate Qualcomm's spectrum into AT&T's existing network. A recent report shows just how far ahead Verizon is in the 4G spectrum race. Including the recent deals Verizon has struck with cable companies, Verizon now has 56% more 4G spectrum than AT&T in the top 10 wireless markets, and 46% more 4G spectrum in the top 100 wireless markets. AT&T needs to find more spectrum, and once again, analysts have brought up Clearwire as the answer, given Clearwire's vast spectrum holdings.A deal between AT&T and Clearwire seems like a good idea. AT&T gains the spectrum it needs for its 4G network, and Clearwire is infused with billions. However, we agree with BTIG that AT&T will not partner with Clearwire, for AT&T has historically preferred to own its spectrum outright rather than just renting it. Unlike Sprint, which has essentially outsourced its 4G strategy to Clearwire, AT&T has historically preferred to retain a higher degree of control over its network, even if it costs AT&T more to do so. Speculation has grown that AT&T will buy Dish (DISH), given its billions in unused spectrum, and less anti-trust worries. Dish has long wanted to enter the wireless market, with its unused spectrum. Since Dish has no wireless customers, we expect much less anti-trust scrutiny.In addition, their limited overlap in the TV industry further highlights the lack of competitive issues. In fact, a Dish acquisition could help AT&T in its negotiations with content providers. But as appealing as a Dish acquisition might seem, we do not think it will occur. For one, it runs counter to Dish's stated strategy, which has been to simply partner with a wireless company, or launch its own network. Secondly, Dish CEO Charlie Ergen has not made any indications he is willing to sell, and given his reputation as a shrewd and tough dealmaker, we think that the price he would be willing to accept is nowhere near what AT&T can pay.

Given AT&T's limited deal options , what can it do? We have a proposed solution that will benefit AT&T, as well as Sprint and Clearwire shareholders. But to understand the rationale behind our proposal, we must first review the relationship between Sprint and LightSquared, seen by many as a competitor to Clearwire.On July 28, Sprint and LightSquared announced a spectrum hosting and network services agreement designed to strengthen both companies. But with the FCC insisting that LightSquared's network interferes with GPS signals, and growing financial issues at LightSquared, this agreement is in jeopardy, even if neither Sprint nor LightSquared will yet admit to it. LightSquared has lost $427 million in the first 3 quarters of 2011, and will most likely run out of cash in the second quarter of 2012 if the FCC does not allow it to launch its network. Since we see no signs of that happening anytime soon, given the issues plaguing the LightSquared's network, we are doubtful that the network will ever launch. Even if the government tests the network according to LightSquared's parameters, it is still not up to standards. And we do not think Philip Falcone and his hedge fund, Harbinger Capital Partners, will be able to come to LightSquared's rescue again. Given that the fund is being investigated by the SEC, and already owns almost all of LightSquared, we do not think that it will be able to invest meaningful sums into LightSquared to keep it afloat. All this leaves Sprint without a partner meant to diversify away from Clearwire. But, we think that diversifying away from Clearwire is a mistake. For the benefit of its own shareholders, as well as Clearwire's, Sprint should radically rethink its relationship with Clearwire.As a reminder, Sprint has a 53.6% economic interest in Clearwire, making it the company's largest shareholder. But, Sprint controls only 49.7% of Clearwire's voting power. Why has Sprint decided on this? Initially, it was to avoid having to bring Clearwire's billions in debt onto its own balance sheet, thus putting Sprint on the hook should Clearwire default. In our first article on Sprint, published on August 31, we praised this arrangement, arguing that it allows Sprint to use Clearwire's spectrum without worrying about default. But times have changed, and in the months since then we have seen just how foolish this arrangement is.Sprint is, in reality, servicing Clearwire's debt, for if Clearwire defaults, its spectrum goes to the creditors, and Sprint's entire 4G network goes with it. One of the primary benefits of the new agreement announced by Sprint and Clearwire on December 1 is that the Clearwire will make a $237 million debt payment, as scheduled. Clearwire's debt may not be on Sprint's balance sheet, but Sprint is still wholly responsible for it. We think that this is absurd, and are calling on Sprint to do what is necessary and acquire Clearwire outright.

Given that Sprint is already the majority shareholder, it has the power to block any takeover, and will do so, for its entire 4G network depends on Clearwire, since Sprint does not have enough spectrum to build a 4G network alone. Sprint is held hostage by Clearwire, and should bite the bullet and takeover Clearwire.

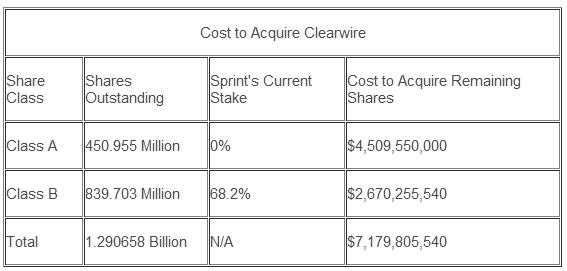

So what should Clearwire be sold for? It owns 46 billion MHz-POP's of spectrum, and has just over $4 billion in debt. Verizon's spectrum deal with Comcast, Time Warner Cable, and BrightHouse valued spectrum at 68 cents per MHz-POP, implying that Clearwire's spectrum is worth $31.28 billion. But lets cut that by 50%, for investors bearish on Clearwire contend its spectrum is not worth what bulls think it is. A 50% discount yields a value of $15.64 billion, and after backing out the Clearwire's $4.019326 billion in debt , we arrive at a total spectrum value of around $11.6 billion. After the recent equity offering , Clearwire has 1.290658 billion shares outstanding, implying that the spectrum is worth $8.97 per share. Adding in the company's other assets and liabilities brings Clearwire's total value to around $10 per share, a 392% premium to current levels. To maximize value for Clearwire and Sprint, we believe that the Sprint should proceed in the following manner:1. Sprint acquires all remaining shares of Clearwire for $10 per share, giving shareholders a huge premium and a profitable exit from the stock. We think that Intel, Google, Comcast, and Clearwire's other strategic investors will sell their shares to Sprint, since they are interested in the growth of 4G service, which will occur no matter who controls Clearwire. Sprint receives around $4 billion in debt, adding to its total, but also receives all of Clearwire's spectrum. As a reminder, Sprint economic interest in Clearwire, as well as its control of Clearwire's spectrum comes not from a majority share of Clearwire itself, but from holding 68.2% of all Clearwire Class B shares. Thus, Sprint controls 49.7% of Clearwire itself via its holdings of Class B common stock. Below we breakdown the cost to acquire Clearwire.

2. Having spent a net amount of $11.19913154 billion to acquire Clearwire (including the assumption of $4 billion in debt), Sprint's balance sheet is now even weaker than before, for it would have to raise most of that amount in the debt markets, further leveraging its balance sheet. However, Sprint would now find itself in the enviable position of having more spectrum than AT&T and T-Mobile combined . Sprint does not need all that spectrum to successfully launch and future-proof its network.Clearwire alone holds more than 5 times the amount of spectrum Verizon and AT&T are using to launch their LTE networks. While Sprint does not need all that spectrum, we know of a certain wireless carrier that does: AT&T. Given that the Justice Department wants to see 4 national players, not 3, it is impossible for AT&T to buy Sprint, and none of the regional carriers have nearly enough spectrum to fulfill AT&T's needs. However, a combined Sprint and Clearwire do.

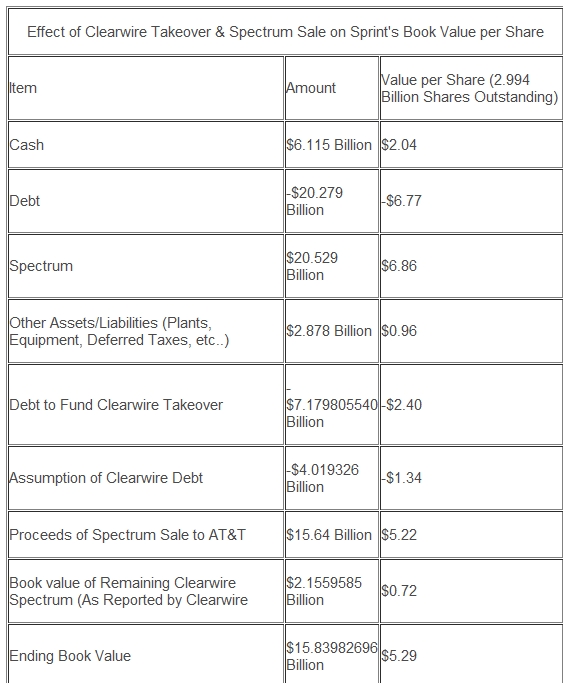

3. Selling excess spectrum to AT&T would be a financial bonanza for Sprint. It knows that AT&T needs spectrum, and given that Dish is unlikely to sell, the only meaningful amount of available spectrum left would be in Sprint's hands. The discount we assigned to Clearwire's spectrum would disappear, in our mind, since Sprint has the upper hand here. We think that Sprint could sell this spectrum for a good deal more than what Comcast, Time Warner Cable, and Bright House sold their spectrum for. AT&T's $39 billion deal with T-Mobile valued T-Mobile's spectrum at a whopping $2.70 per MHz-POP for T-Mobile's 14.4 billion MHz-POP. But, AT&T stood to gain millions of customers and cell towers as well, so valuing Clearwire's spectrum at that level is unreasonable. We will use a valuation of 68 cents per MHz-POP, which is what Verizon paid for its spectrum from Time Warner Cable, Comcast, and Bright House. For the record, we think that Clearwire's spectrum can be sold for a lot more, given that Clearwire is the last major source of available spectrum left in the wireless market. However, we will be conservative in our valuation. Sprint currently uses nowhere near half of Clearwire's spectrum, so selling half of Clearwire's spectrum to AT&T would still allow Sprint to effectively deploy its LTE network and leave enough room for an inevitable rise in future data demand. A GigaOm story about Sprint's 4G network highlights a piece of an interview with Clearwire CTO John Saw. In that interview, "Saw said Clearwire plans to start off with 20 MHz carriers, double the bandwidth of what Sprint’s own LTE radios will be able to pump out. That would allow Sprint and Clearwire’s to match, if not exceed, AT&T’s and Verizon's capacity in the areas where TD-LTE deployed. But Clearwire doesn't have to stop there. It has enough spectrum to launch that same 20 MHz carrier three or four times over. Customers in those ‘mega-cells’ would have share access to hundreds of Mbps of bandwidth, overshadowing anything Verizon and AT&T can do with the spectrum holdings they have today." A combined Clearwire and Sprint have more than enough spectrum to guarantee the network works just as good, if not better than their rivals, and they would still have vast amounts of unused spectrum. Selling 23 billion MHz-POP's at 68 cents each would give Sprint $15.64 billion. By doing so, Sprint recoups all of the $11.2 billion paid for Clearwire, and is able to retire over $4 billion of its legacy debt. And Sprint is still left with the spectrum it needs to build its LTE network. Sprint's book value, even using conservative measurements, would rise by a fairly large amount. For the record, Sprint's tangible book value per share at the end of the third quarter was $3.67.

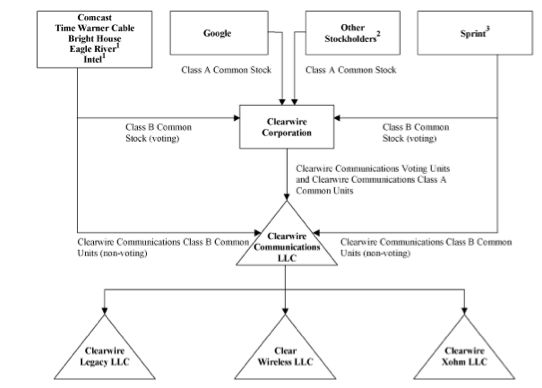

The major risk to this proposal is whether or not Sprint can in fact sell spectrum to AT&T at 68 cents per MHz-POP (or higher). We think Sprint can, due to the fact that AT&T cannot simply acquire Clearwire on its own. This is because of the extremely convoluted nature of Sprint's relationship with Clearwire, which is illustrated below.

Clearwire's spectrum is housed in Clearwire Communications LLC, the majority of which is controlled by Sprint. In the recent equity raise, Sprint purchased enough shares to maintain its stake in Clearwire at previous levels. As per Clearwire's bylaws , the remainder of Clearwire Communications stock is held by the other holders of Clearwire's Class B common stock, and by acquiring all Class B shares of Clearwire, Sprint takes control of all remaining shares in Clearwire Communications as well. This is why Sprint cannot simply up its stake to 50.1%. To gain full control over Clearwire's spectrum, Sprint must purchase all of Clearwire's stock, so that it controls 100% of Clearwire Communications. While Clearwire can still sign operating agreements with other companies, it cannot simply sell the spectrum outright, for Sprint can block such a transaction, just as it can block a whole takeover of Clearwire. But, Clearwire still has leverage over Sprint, since Sprint controls only 49.7% of the voting power of Clearwire itself. We have never seen such an arrangement before, where a company (Sprint) controls the key assets of another company (Clearwire), but does not control the company itself (Clearwire). Clearwire cannot sell itself, because it does not have majority control of its own spectrum. Clearwire's debt is backed by its spectrum , and if Clearwire chooses to default on its bonds and declare bankruptcy, bondholders seize control of the spectrum and can then proceed to sell it, costing Sprint its 4G network. Clearwire shareholders are protected because any spectrum sale will generate far more than $4 billion, meaning anything over that amount goes to the shareholders.We think that this series of transactions would be able to pass anti-trust scrutiny, for it leaves 4 national carriers, and the FCC knows that AT&T needs spectrum from somewhere. Both have called on Congress to begin the process to auction off more spectrum, but that will be a long journey. Until then, AT&T must get more spectrum to be able to effectively compete with Verizon, and the only meaningful owner of spectrum left who is willing to sell is Clearwire. AT&T would receive 23 billion MHz-POP's of spectrum, almost 60% more than in the T-Mobile deal, for $7.5 billion less. A Sprint takeover of Clearwire benefits Clearwire investors, who can finally see Clearwire's true worth validated.Sprint benefits because it gains access to the spectrum it needs to operate its LTE network, as LightSquared's future looks increasingly bleak. Furthermore, by selling spectrum to AT&T, Sprint's own financial condition improves. Sprint's tangible book value per share jumps to $5.29, a 44% increase from current levels. Sprint is infused with billions in cash, allowing it to retire billions in debt and bolster its balance sheet. And AT&T benefits because it gains the spectrum it needs to compete with Verizon.

The past few months have dramatically altered the wireless landscape. Verizon has bough billions in spectrum as AT&T and T-Mobile fought to salvage their agreement, and Sprint bailed out Clearwire yet again. But now, we see a unique opportunity for Sprint and Clearwire to unlock billions in value for their shareholders, and for AT&T to acquire the spectrum in needs to compete effectively in the new wireless market. This proposed transaction benefits all the participants in some way, and we think it is a sensible path for the companies to take.

0 Comments

Recommended Comments

There are no comments to display.